Money stress hits different when you have a family depending on you. I remember the first time I sat down to actually budget for my household — I had no idea where half our money was going. Groceries felt way higher than they should be, and by the third week of the month, we were always tight. Sound familiar?

If yes, you are not alone. Most families never had someone sit them down and show them how to build a real budget. Not a fancy spreadsheet with formulas nobody understands — just a simple, honest plan that shows where your money goes and how to make it work for you.

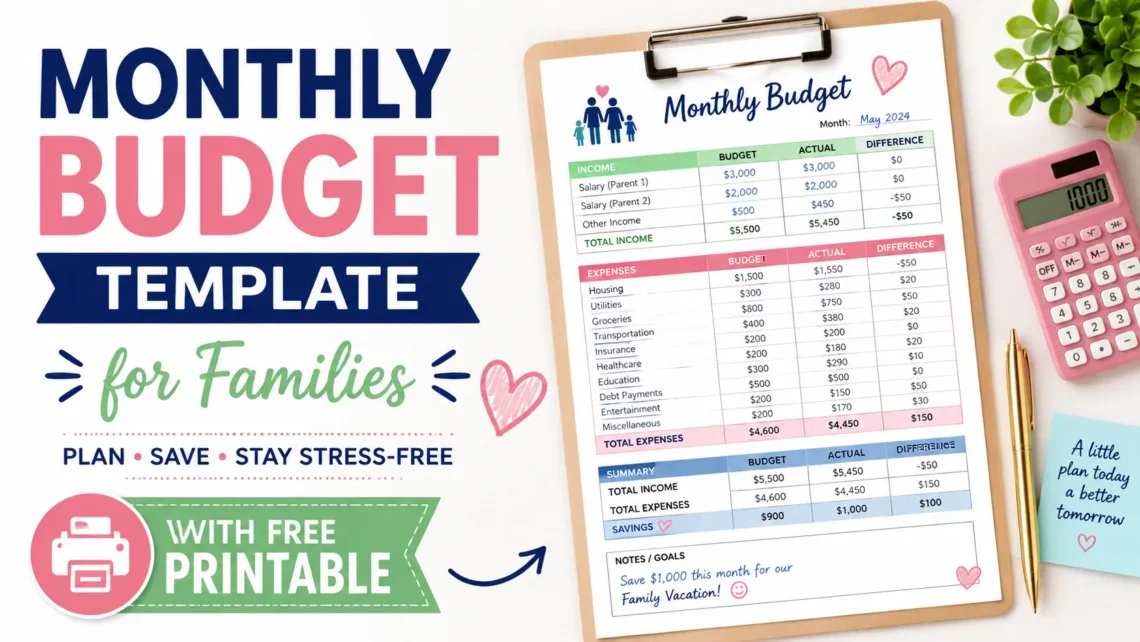

This guide gives you a complete monthly budget template for families, a free printable version, and a real-life example so you can see exactly how it works in practice.

Quick Answer: What Is a Family Budget Template?

A family budget template is a simple document (paper or digital) that lists all your household income and expenses for the month. It helps you see, at a glance, whether you are spending more than you earn, where your money is leaking out, and how much you can save. A good template splits expenses into categories like housing, food, transportation, kids, savings, and fun money.

Why Most Family Budgets Fail

Before I give you the template, let me tell you why so many family budgets don’t last past month one.

I have seen this pattern over and over, and I have lived it myself. Families make the budget too strict. They cut out everything fun in the first month, feel deprived, and quit by week two. Or they forget to include irregular expenses — things like car insurance, school supplies, or birthday gifts — and then the budget “breaks” the moment one of these shows up.

A budget that works has to be realistic. It needs room to breathe. That is the whole idea behind the template below.

The Monthly Budget Template: Core Categories

Here is the structure I recommend for most families. You can adjust the percentages based on your city and situation, but this gives you a solid starting point.

| Category | Suggested % of Income | What It Covers |

|---|---|---|

| Housing | 25-30% | Rent/mortgage, property tax, HOA fees |

| Utilities | 5-8% | Electricity, water, gas, internet, phone |

| Groceries | 10-15% | Food, household supplies |

| Transportation | 10-15% | Car payment, gas, insurance, public transit |

| Kids/Childcare | 5-15% | Daycare, school fees, activities, supplies |

| Insurance & Healthcare | 5-10% | Health insurance, medical bills, prescriptions |

| Debt Payments | 5-15% | Credit cards, student loans, personal loans |

| Savings | 10-20% | Emergency fund, retirement, college fund |

| Fun Money | 5-10% | Dining out, entertainment, hobbies |

| Miscellaneous | 3-5% | Gifts, donations, unexpected costs |

These percentages will not fit every family perfectly, and that’s okay. If you live in a high cost city, housing might eat 35% of your income and that’s just reality. The point of the template is not to hit exact numbers — it’s to give every dollar a job before the month starts.

How to Create a Family Budget That Works (8 working tips)

Real-Life Example: The Martinez Family Budget

Let me walk you through an example so this feels real instead of just theory.

Meet the Martinez family — Daniel and Priya, with two kids, ages 6 and 9. Daniel works as an electrician and Priya works part-time from home. Their combined monthly take-home pay is $5,800.

Here is how they broke it down:

Income: $5,800/month

- Housing (rent): $1,600 (28%)

- Utilities: $380 (7%)

- Groceries: $700 (12%)

- Transportation: $650 (11%)

- Kids (daycare + activities): $500 (9%)

- Insurance & healthcare: $420 (7%)

- Debt payments (car loan): $350 (6%)

- Savings (emergency fund + retirement): $800 (14%)

- Fun money: $300 (5%)

- Miscellaneous: $100 (2%)

Total: $5,800

Notice something? Every single dollar has a place to go. That is the real secret behind budgets that actually work. When Daniel and Priya first started, their groceries were closer to $950 a month. They found this out only after tracking three weeks of receipts — turns out a lot of it was impulse buys and eating out disguised as “quick grocery runs.” Once they saw the number in black and white, cutting it down to $700 felt natural instead of forced.

This is something I have noticed in almost every family budget I have looked at: groceries and eating out are usually the biggest hidden leak. Not because people are careless, but because these purchases happen in small amounts, spread across the whole month, so nobody notices the total until they add it up.

Practical Scenario: What Happens When Something Unexpected Comes Up

Budgets are easy on paper. Real life is messier. Let’s say the Martinez family’s car needs a $400 repair in the middle of the month. What happens?

This is exactly why the “Miscellaneous” and “Savings” categories exist. If they have an emergency fund already set aside (even $500-1000 to start), this repair does not derail the whole month. They pull from savings, replace it next month, and move on. Families without this buffer usually end up on a credit card, and that $400 repair turns into $460 after interest by the time they pay it off.

My honest observation after seeing this play out many times: the emergency fund is not optional. It’s the piece that keeps the whole budget from falling apart the first time life throws a curveball. Even $30 a week adds up to over $1,500 in a year.

Step-by-Step: How to Build Your Own Family Budget

Step 1: Write down your total monthly income

Include everything — salary, side income, child support, freelance work. Use the number after taxes (take-home pay), not before.

Step 2: List every expense from last month

Pull up your bank and credit card statements. Write down every category, even the small ones like coffee or subscriptions. This step is uncomfortable but it’s the most honest look you’ll get at your spending.

Step 3: Sort expenses into categories

Use the table above as your guide. Group similar expenses together.

Step 4: Compare income vs expenses

If expenses are higher than income, this is where you find what to trim. Start with the categories that feel less essential — fun money, subscriptions, eating out — before touching housing or debt payments.

Step 5: Set your savings goal first, not last

Most people budget savings as “whatever is left over,” and that usually means nothing is left over. Flip it — decide your savings amount first, then build the rest of the budget around it.

Step 6: Review every two weeks

A budget is not a “set it once” document. Check in every payday to see if you’re on track, and adjust as needed.

Also read:

Family Financial Planning Guide Every Parent Should Read

Free Printable Monthly Budget Template

I put together a simple printable version you can use right away. It includes:

- A monthly income tracker

- Expense categories with blank fields to fill in

- A savings goal tracker

- A section for irregular/one-time expenses

- A weekly check-in box

Print it out, stick it on the fridge, or keep it in a binder. Some families prefer a shared spreadsheet, but I have found that a physical printable works better for many households because everyone can see it — kids included. When your children see the budget, they understand “no” a little better, and that alone can cut down on a lot of small requests at the store.

Common Mistakes to Avoid

Forgetting irregular expenses. Car registration, school fees, holiday gifts — these show up once or twice a year but wreck a monthly budget if you don’t plan for them. Divide the yearly cost by 12 and set that amount aside every month.

Being too strict too fast. Cutting all fun spending in month one usually backfires. Leave room for a little joy in the budget.

Not involving the whole family. Budgeting works better when both partners (and even older kids) understand the plan. Money fights often come from one person feeling left out of financial decisions.

Ignoring small recurring charges. Subscriptions add up fast. Streaming services, apps, memberships — review these every few months and cancel what you don’t use.

Frequently Asked Questions

How much should a family spend on groceries per month?

Most families spend between 10-15% of their take-home income on groceries. For a family of four earning around $5,800/month, that’s roughly $580-$870, though this varies based on location and dietary needs.

What is the 50/30/20 budget rule for families?

This rule splits income into 50% needs (housing, food, bills), 30% wants (fun money, entertainment), and 20% savings and debt payments. It’s a simple starting point, though families with kids often need to adjust these percentages since childcare and school costs can take up more room.

How much emergency fund should a family have?

A good starting goal is $1,000, then build up to covering 3-6 months of essential expenses. Start small — even $25-50 a week adds up over time.

Should couples combine finances or keep them separate?

Both approaches can work. Some families combine everything into one household budget, while others keep individual accounts and split shared bills. What matters most is that both partners are on the same page about the family’s overall financial goals.

How do I stick to a budget with kids who have different needs?

Build a per-child line item into your budget for activities, clothes, and school costs. This prevents one child’s expenses from quietly eating into money meant for the whole family.

Final Thoughts

Building a family budget is not about perfection. Some months will go over in one category and under in another — that’s normal life, not failure. What matters is that you and your family know where the money is going and you’re making decisions on purpose instead of by accident.

Start with the template above, adjust it to fit your real numbers, and give it a few months before judging whether it works. Most families I’ve seen succeed with budgeting are the ones who kept adjusting instead of giving up after one hard month.