Okay so let’s talk about the house fund.

You know the one. That savings account you keep meaning to “really focus on” once things calm down. Once the car is paid off. Once the kids stop needing new shoes every four months (spoiler: they never stop). Once life gets less expensive, which, lol, when has that ever happened.

Here’s the thing though. My husband and I spent almost two years saving for our down payment, and the single dumbest mistake we made had nothing to do with how much we saved. It was where we kept it.

For the first year, our down payment money just sat in the same savings account we’d had since we opened our first joint account together. You know, the boring one at the big bank down the street, the one that mails you a paper statement nobody reads.

It was earning something like 0.3% interest. I didn’t even know that number existed until I actually looked it up one night out of curiosity and nearly spit out my coffee.

Thirty thousand dollars sitting there for a year earned us less than a hundred bucks in interest. A HUNDRED BUCKS. Meanwhile my cousin, who I love dearly but who has never once beaten me at Scrabble, mentioned offhand that her house fund was earning her over a grand a year just sitting there doing nothing.

Doing NOTHING. Not budgeting harder. Not clipping coupons. Just… sitting in a different account.

I felt like an idiot. A well-meaning, hardworking idiot, but an idiot nonetheless.

So let’s save you that face-palm moment. Here’s everything I wish someone had grabbed me by the shoulders and told me before we started saving for our house.

Rule #1: Your Down Payment Fund and Your “Oops I Need Groceries” Fund Should Never Live Together

This sounds obvious written down, but you’d be shocked how many people (raises hand, guiltily) keep their house money in the same account they use for everyday spending.

Here’s why that’s a problem: money is sneaky. It hides in plain sight. If your down payment cash and your grocery money and your “we’re getting takeout because today was too much” money are all mixed together in one account, you will absolutely dip into the house fund without meaning to. Not because you’re irresponsible. Because you’re human, and $4,200 just looks like a number you have, not a number that’s spoken for.

We opened a completely separate high-yield savings account the day we got serious about buying. Different bank, different app, out of sight. It became almost like a locked box in my brain. That money wasn’t “ours to spend,” it was “ours to become a house.”

Rule #2: A High-Yield Savings Account Is Not a Scam, I Promise

I know, I know. “High-yield” sounds like one of those things your uncle brings up at Thanksgiving right before he tries to sell you on a pyramid scheme. It’s not that. It’s just a regular savings account, protected the exact same way your current one is (FDIC insured, meaning the government backs it up), except it actually pays you something for the privilege of holding your cash.

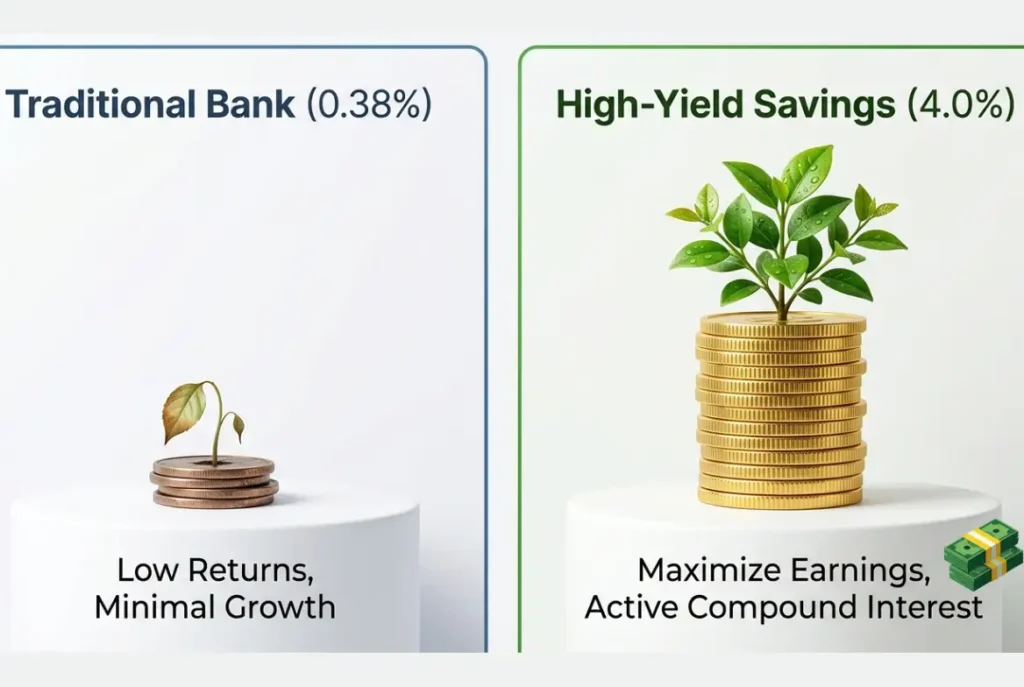

Right now, in mid-2026, the good ones are paying somewhere around 4-5% APY. Compare that to the roughly 0.38% national average most people are stuck earning without realizing it, and you start to see why this matters.

Let’s make it real. $30,000 sitting in:

- A typical bank savings account (0.38%): earns you about $114 a year

- A solid high-yield savings account (4%): earns you about $1,200 a year

Same $30,000. Same effort. Over a thousand dollars difference. That’s basically a free plane ticket, or your closing costs halfway covered, or a really nice couch for the new living room. For doing absolutely nothing except picking a better place to park your cash.

Family Financial Planning Guide Every Parent Should Read

Rule #3: Automate It So You Don’t Have to Rely on Willpower (Because Willpower Is Overrated)

I used to think saving was about discipline. Turns out it’s mostly about laziness, in a good way.

The month we set up an automatic transfer of $600 every payday straight into the house fund, everything changed. Not because we suddenly became more disciplined people. Because we removed the decision entirely. The money moved before we ever saw it, so we never had the chance to talk ourselves out of it.

Contrast that with the months we tried to “save whatever’s left over.” You know what’s left over at the end of most months? Nothing. There’s never anything left over. Left-over money is a myth, like a healthy relationship with the office vending machine.

Pay the house fund first. Treat it like a bill you owe your future self.

Rule #4: Match Your Account to How Soon You’re Actually Buying

This one took me embarrassingly long to figure out.

If you’re buying within the next year, keep everything liquid. A high-yield savings account or money market account, full stop. You need to be able to grab that cash the second an offer gets accepted.

If you’re two to three years out, you can get a little fancier. We eventually split part of our fund into a CD ladder, basically staggering a few certificates of deposit at different lengths (6 months, 12 months, 18 months) so part of the money is always coming due, always ready, but a chunk of it is earning a slightly better locked-in rate the whole time.

If you’re three-plus years out, sure, maybe a small slice goes somewhere with a bit more growth potential. But I want to be honest with you here: don’t get cute with your down payment money in the stock market. I’ve seen friends do this. I’ve seen the market take a nosedive six months before they wanted to buy, and suddenly their timeline got pushed back two years. Down payment money should be boring. Boring is the whole point.

Rule #5: You Might Not Need as Much as You Think

Everybody assumes 20% down is the golden rule. It’s not, it’s just the number that gets repeated the most.

Depending on your loan:

- Conventional loans can go as low as 3-5% down

- FHA loans often only need around 3.5%

- VA and USDA loans can sometimes mean 0% down if you qualify

This changes everything about your goal. Chasing $70,000 when you actually only need $35,000 is exhausting and, frankly, unnecessary. Do the math for your actual situation before you set a number that might be scaring you into procrastinating.

(Quick heads up though: anything under 20% down on a conventional loan usually means PMI, an extra monthly cost until you build equity. So it’s not a totally free lunch, just a faster path to the table.)

Rule #6: Don’t Forget the Closing Costs Ambush

This one bit us. We saved exactly our down payment number and felt very proud of ourselves, and then closing costs showed up like an uninvited guest who eats all your chips. Budget an extra 2-5% of the home price for this. Nobody tells you this loudly enough.

So, Where Does This Leave You?

Honestly? Pick a high-yield savings account this week. Not next month, not “when I have time to research it properly.” This week. Open it, separate it from your everyday money, set up an automatic transfer even if it’s small, and let it sit there quietly earning more than you’re used to.

You don’t need a finance degree. You don’t need a spreadsheet with fourteen tabs (though hey, if that’s your thing, no judgment). You just need your money in a smarter room than it’s currently sitting in.

We closed on our house fourteen months after we made that one switch. Was the better interest rate the only reason? No. But it definitely didn’t hurt, and it made the whole process feel less like white-knuckling it and more like we actually had a plan.

Your future front door is waiting. Go give your money a better place to sit while you get there.

Not financial advice, just one household’s lessons learned the semi-hard way. Rates mentioned are current as of mid-2026 and will change, so compare current offers before you open anything.